The innovative insurance company capitalizing on artificial intelligence, Lemonade Inc. (LMND) has been on a bumpy ride with shares 87% farther from all-time highs. While many challenges still exist amid the persistent financial net losses and wider tech sell-off, the company has been making substantial progress and growing nicely.

The latest earnings report from the fintech company brought about both good and bad news causing the stock to run wild with an uptick followed by a downtrend. While investors initially celebrated the beat earnings and revenue along with improvement across most metrics, they later started worrying about its underwriting which is still much farther from the target 75% loss ratio. The earnings proved hard to digest for investors as they remained uncertain whether to be happy about the much progress or concerned about the challenges ahead.

On May 18, LMND stock was down by 3.69% in the premarket to trade at $20.38 at the time of writing. This downtrend came after the stock surged by 9.41% in the prior trading session which had it valued at $21.16 a share.

Let’s have a look at the bright and not-so-bright side of the latest earnings report shared on May 9, 2022.

LMND’s Q1 2022 Performance

On the Bright Side

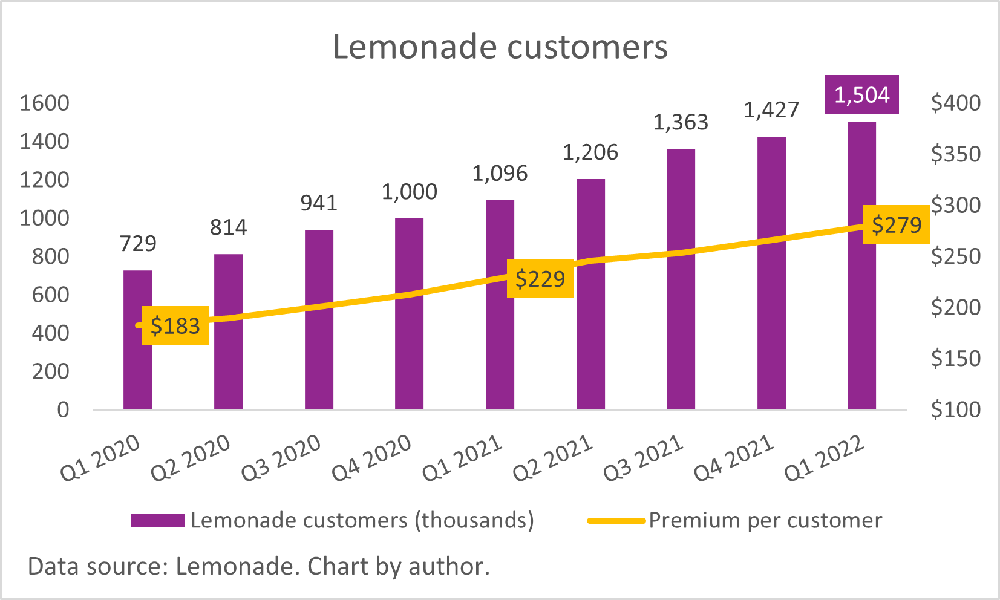

According to the financial results, the fintech company’s business grew impressively in the first quarter with in-force premiums climbing 66% YOY. A 37% increase in the number of customers on top of a 22% increase in premium per customer resulted in in-force premiums of $419.0 million in Q1 2022. Thus, with a customer count of 1,504,197, the premium per customer reached $279 at the end of the quarter. Subsequently, gross earned premiums surged 71% YOY to $96 million.

Furthermore, marking a stark 88.5% increase in YOY was LMND’s revenue which came at $44.3 million against the prior year’s $23.5 million. The quarterly revenue beat the consensus estimate by 2.43%.

On the earnings front, the company came out with a loss of $1.21 per share against the expected $1.43 a share. The loss widened from the comparable period’s $0.81 per share but was better than expected.

The adjusted gross profit soared by 226% YOY while the cash, equivalents, and investments were $1.01 billion at the end of the quarter.

No-So-Bright Side

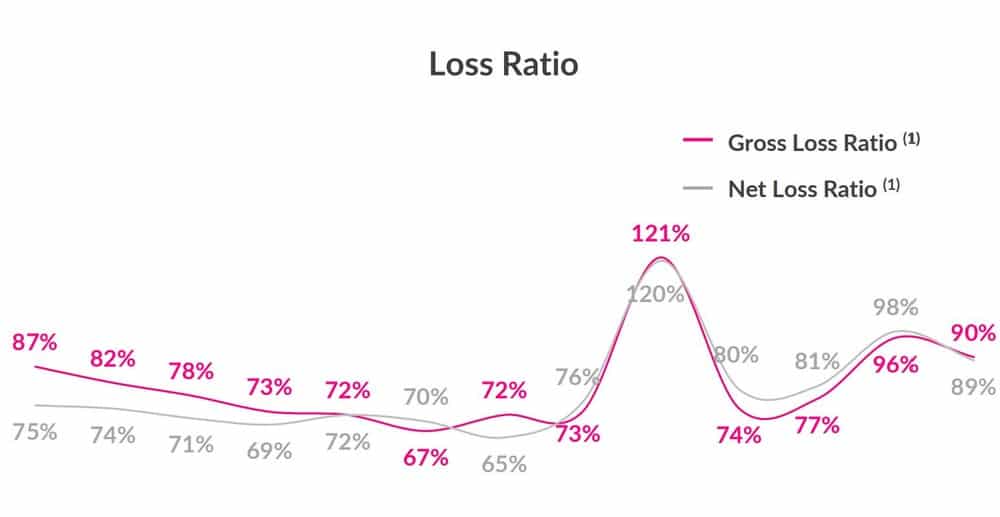

Raising concerns was the company’s underwriting i.e. its loss ratio which demonstrates how much of a policy it pays in claims. While the loss ratio did show some improvement YOY at 90% against 121% last year, it is still very far from its target of 75%.

The metric had been improving sequentially before last year’s Q1 which brought a big challenge to the continued improvement due to the Texas freeze. CEO Dan Schreiber attributed the still vast loss ratio to inflation causing a rise in claim payouts amid the lagging policy rate increase, in the letter to shareholders.

Moreover, total operating expenses rose 68% YOY to $92.5 million due to higher expenses in general and technology development. Consequently, the adjusted EBITDA loss also widened to reach $57.4 million against the comparable $41.3 million.

Thus, with the higher loss ratio, and increasing operating and EBITDA losses, LMND will surely run out of cash soon even if the sum is large.

LMND’s Future Guidance

Due to the Russia-Ukraine conflict, geopolitical and economic turmoil, and peaking inflation on top of rising interest rates, the company (excluding the Metromile acquisition set for Q2 2022) expects:

| Q2 2022 | Fiscal 2022 | |

| In Force Premium | $445-$450 million | $535-$545 million |

| Gross Earned Premium | $103-$105 million | $426-$430 million |

| Adjusted EBITDA | $(70)-$(65) million | $(280)-$(265) million |

| Revenue | $46-$48 million | $205-$208 million |

Analysts were forecasting $51.35 million in Q2 revenues and $213.48 million for the full year. However, the pending acquisition of Metromile in the ongoing quarter would accelerate Lemonade Car rollout and contribute to its financials which was not included in the company guidance.

Conclusion

The AI-powered fintech company while showing promising progress and continuous improvement still lags on certain key metrics. While it expects to bring down the loss ratio to 75%, it is still far off at 90% and the company’s 2022 guidance also came below the expected. Otherwise, the company has been demonstrating high growth and improved performance YOY. Moreover, with the Metromile acquisition in sight, LMND might just produce better-than-expected financials if it continued to bring down the loss ratio and shrinks net loss.